Much has been written about how finance organizations can become strategic partners with the businesses they support. While purported experts point to a variety of frameworks, scorecards and key performance indicators, etc. as the keys to bridging the gap between finance and business, these trite ‘solutions’ have done little to make finance the strategic business partner it seeks to be.

This is a guest post from Anand Sanwal. Read more about the author at the end of this article.

Given the time, money and effort spent, you may be a bit demoralized and even speculating that the finance-business chasm cannot be crossed. Paradoxically, the link between finance and the business has been under finance’s proverbial nose for some time – resource allocation.

A serious concerted effort to optimize an organization’s resource allocation ultimately enables finance to develop the bridge between finance and strategy. This discipline known as corporate portfolio management works to actively manage the company’s resource allocation as a portfolio of discretionary investments.

All companies allocate their resources – very few optimize their resource allocation. Finance is uniquely positioned to enable this because they sit at the nexus of information and data required to undertake a corporate portfolio management effort. (Note: Corporate portfolio management is often referred to by different terms so as a point of reference, terms such as IT portfolio management, enterprise portfolio management, product portfolio management, project portfolio management, resource allocation and investment optimization are similar. In fact, these all are slices or subsets of corporate portfolio management.)

From Resource Allocation to Strategy

First, it is worth understanding the tie between resource allocation and strategy – they are the same. Where you allocate your resources is your strategy. PowerPoint presentations, speeches by senior leadership, strategy bullets nicely framed on a wall, etc. are all interesting and potentially useful, but they are not your organization’s strategy.

For instance, if your stated corporate strategy is to have the most engaged and loyal customers (this sounds good, right?), but you allocate all your investment dollars to acquiring new customers, your strategy is actually around customer acquisition. This is a very simple example but clearly demonstrates the dichotomy that can and often exists between a stated and real strategy.

A great article entitled “How Managers’ Everyday Decisions Create – or Destroy – Your Company’s Strategy” that appeared in the Harvard Business Review (February 2007) nicely articulated the connection between resource allocation and strategy and also pointed to the need for a corporate portfolio management discipline.

“How business really gets done has little connection to the strategy developed at corporate headquarters. Rather, strategy is crafted, step by step, as managers at all levels of a company – be it a small firm or a large multinational – commit resources to policies, programs, people and facilities. Because this is true, senior management might consider focusing less attention on thinking through the company’s formal strategy and more attention on the processes by which the company allocates resources.”

The upshot of this is that if finance can enable the process to enable better resource allocation (which is strategy), they will have succeeded in becoming a de facto strategic partner to the business.

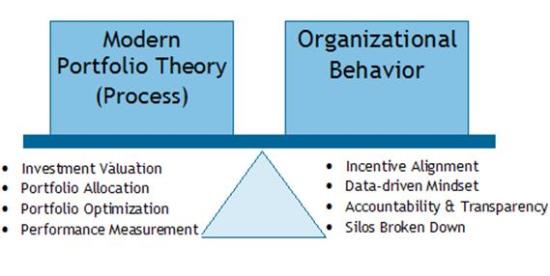

The Two Levers of Corporate Portfolio Management

So now the question turns to how to build a corporate portfolio management discipline and ensure its success. A successful corporate portfolio management effort is predicated on two dimensions.

Two Levers of Corporate Portfolio Management

Modern Portfolio Theory (aka the process)

This is what people generally think of when they think of corporate portfolio management. It is comprised of:

- Investment valuation – This includes defining what an investment is. It is worthwhile to take an expansive definition of what comprises an investment because this is not just capital expenditures (capex), but also should include operating expenses (opex). In general, 25-40% of an organization’s expenses are discretionary and hence are investments. Investment valuation also requires consistency of valuation methodology which necessitates using driver-based models to create projections and also looking at past NPVs and ROIs to consider strategy and other qualitative aspects that drive investment ‘value’.

- Portfolio allocation – This requires determining investment areas/themes and the associated allocations. Basically, what are my strategic priorities for investment and how much will go to each area? For example, 25% in customer acquisition, 20% in IT, 55% in customer retention. The allocation should also consider the risk profile of investments, e.g., 60% in low risk, 30% in medium risk and 10% in high risk.

- Portfolio optimization – This requires selecting the best investments to support the portfolio allocation and periodically rebalancing the portfolio to ensure consistency with desired portfolio allocations. The aim is to maximize strategic and financial return per unit of risk.

- Performance measurement – A key element of successful corporate portfolio management is capturing actual investment results to enable promise vs. performance. Doing this ultimately lets an organization improve ongoing investment valuation based on actual results and allows it to rebalance the portfolio based on performance achieved.

Most people with a finance background will recognize the above tenets of portfolio theory. The problem with most of the discussion of corporate portfolio management is that it assumes that people behave according to a theoretical/rational construct.

While various experts like to offer platitudes saying things like, “Just manage your company’s investments like you manage your own investments,” they fail to realize that many individuals may not even manage their own personal portfolios as they should.

They may know what they should do but emotions, intuition, and other external influences take them off this rational path. What often leads us astray in our personal portfolio is what leads us astray in an organizational setting – behavior.

The challenge in an organization is magnified by the fact that it is hundreds or thousands of people whose behavior that needs to be considered. And so this is the second fundamental lever of corporate portfolio management – organizational behavior.

Organizational Behaviour

In order to optimize one’s corporate portfolio, the behavioral elements must be understood with:

- Data-driven mindset – Organizations often make decibel- or intuition-led decisions and corporate portfolio management, like 6-Sigma, requires data and analytical decision making.

- Silos removed – Corporate portfolio management success requires people thinking about what is best for the organization and not just what is best for “my world” – silos and organizational dynasties need to be broken down.

- Incentive alignment – People should be motivated by similar short- and long-term incentives.

- Accountability & transparency – There should be a willingness to share information and effectively create a marketplace for investments.

Moving organizational behavior is the larger challenge and this takes time to change. At American Express, we have actively worked on changing organizational behavior and have made significant inroads over time, but it has not happened overnight. We have conducted cross unit investment reviews, sponsored an internal corporate portfolio management conference and even created a resource allocation simulation to visibly demonstrate the benefit of corporate portfolio management.

Bringing Corporate Portfolio Management to Your Organization

If you think corporate portfolio management can be implemented in one month or one quarter, it is not for you. Corporate portfolio management is not a sprint and requires the will and heart of a marathoner. You will see benefits along the way, but it takes time to realize the full potential of a well developed corporate portfolio. But once defined and running, an actively managed corporate portfolio management discipline will pay immeasurable dividends.

For American Express, we can point to stock price out-performance over our benchmark indices as well as our competition since adopting corporate portfolio management. Our resource allocation effectiveness also helps to drive our PE multiple (price to earnings multiple), which is significantly larger than our competitive peers.

Very tactically, the corporate portfolio management discipline has helped us understand what businesses we should exit and where we might want to invest more. It has enabled us to reallocate money across business segments for the first time which can be very challenging in large organizations.

Most importantly, corporate portfolio management has become part of the DNA of the organization with finance and the business talking about their investments on an ongoing basis. Finance leads the corporate portfolio management effort but with significant and very direct input and interaction with the business.

The chasm between finance and the business has been bridged by utilizing corporate portfolio management, and the benefits to the organization in terms of financial and strategic performance as well as employee engagement have been significant.

If you are serious about making finance a strategic partner with the business, and if you finally want to make some forward progress after being on the treadmill for so long, corporate portfolio management offers you a solution to this intractable problem. It requires effort and patience, but, as evidenced by American Express, it can close the finance and business gulf and ultimately generate outstanding performance.

Anand Sanwal is the Vice President, Investment Optimization and Strategic Business Analysis, at American Express where he is responsible for managing the company’s corporate portfolio management effort – widely recognized as the most ambitious corporate portfolio management undertaking to date. In his role, he also oversees the CFO’s strategic planning group. He is also the co-founder of the Corporate Portfolio Management Association (http://www.corporateportfoliomanagement.org).

He is the author of the book Optimizing Optimizing Corporate Portfolio Management: Aligning Investment Proposals with Organizational Strategy (Wiley, April 2007) and is a recognized thought leader on corporate portfolio management speaking frequently to companies and research organizations including the Beyond Budgeting Round Table, CFO Executive Board, Enterprise Portfolio Management Council, and Gartner amongst others. He is also the holder of a portfolio management patent.

Thoughts and additional discussion on corporate portfolio management are found at Anand’s blog (http://www.corporateportfoliomgmt.typepad.com). He can be reached at anand@anandsanwal.com.