|

|

| themanager.org | Search |

Myths - STP in Financial Services

Author: Deepak Pareek, FinaTech India

Summary:

What is STP, its’ benefits and strategies to have best solutions? Is the business case for STP still valid and what should be the key elements in an STP strategy? What are the myths surrounding the importance of STP.

This article takes a look at the subject of STP by attempting to underline its importance, best way forward and in the process, exploding a few of the myths associated with it.

Introduction

Straight through processing had been a subject of keen interest in the securities industry over the past few years, and as such received a lot of attention from market players, IT vendors and service providers.

What it is

Straight through processing (STP) is the end-to-end automation of the trading processes both within and between buy and sell side institutions. In short, it is a vehicle to real-time stock/ trade processing in Financial Service industry, with a seamless integration of components and processes involved in the trading cycle starting from first request to buy/sell interest ending up to trading settlement and reporting.

It starts from the first capture of an order through to final settlement. It involves the seamless, electronic transfer of information to all parties involved in the trading cycle utilizing standardized information flows, technologies, and infrastructures.

STP provides wired links for investment managers and ability to process trade without manual intervention and exception, thereby eliminating chances for human errors. In short, T+1 is the simple term for the process of clearing and settling a trade one day after the trade date.

Advantages

The present trade lifecycle is a maze of manual and electronic processes, taking several days, typically three to five days, from initiation to settlement. STP does it all electronically without the need for re-keying or manual intervention. Today, when an investor (individual or corporate) makes a trade, the order starts a complex procedure that extends over a few days. Phone calls and other paper documents fly back and forth between various players like broker/dealers, asset managers, etc. This complex set of operations is true even for a relatively simple domestic retail equity order. The complexity increases for a cross - border trade before it’s finalized.

It is a known fact that as trading volumes explodes, failure rates increase, which in turn, degrades the quality of customer service. To a customer, the ability to achieve a fully integrated STP capability enables greater access to liquidity with a service linking all the areas of the investment chain. STP, in its entirety, is expected to provide all affected financial services players with tremendous benefits, including greatly shortened processing cycles, reduced risk and lower operating costs. In addition, STP reduces errors through lost or wrongly input orders, speeding settlement, reducing risk, and cost of capital.

One of the key drivers of this interest was the T+1 initiative, originally conceived by SIA, the American Securities Industry forum, to address potentially increasing trading volumes in the US securities market. It was anticipate that, STP solutions would be needed to meet the global demand that has resulted from the explosive growth of online trading. They are also required to help financial markets firms achieve one-day trade settlement (T+1). The financial players must heed the U.S. Securities and Exchange Commission’s call for T+1. Of late, with the shelving of the T+1 initiative and the indifferent post - 9/11 business climate in the financial services industry, STP plans appear to have been relegated to the backburner.

Impacted players:

Every player in the trade cycle will be affected in this process. Investors (Retail customers), Fund Managers, Broker/ Dealer, Custodian, Clearing Agents, Stock Exchange, Investment Managers, Credit rating agencies, Electronic Transaction Network, Information Providers (Electronic & others), Regulatory Bodies, Vendors are a few of the chain of players who would definitely be affected.

Benefits

- Improved trade process

- Reduced risk exposure

- Efficiencies of electronics and scale

- Higher volumes

- Greater accuracy

- More customer satisfaction

- Global competitiveness by enhancing post-trade processing and settlement

- Support for increased volumes

- Synchronization of the clearance and settlement process across asset classes

- Enabling more fungible, flexible trading and investing

Keys to implementation process

A suggested practical implementation of STP involves a number of processes:

- Order processing - from indications of interest through to order routing, order execution and order confirmation

- Links - between the front, middle and back offices

- Links - to clearing and settlement, custody and safekeeping

- Connectivity - customer and supplier connectivity at every stage

Is the business case for STP still valid and what should be the key elements in an STP strategy?

1. STP is about T+1

One of the biggest myths is that STP was all about T+1 and thus, with the indefinite postponement of that initiative in the US markets, no longer an important initiative.

But STP does not just concern the US securities companies but pervades the entire globe and gamut of financial services processes, not just the trading and settlement related processes.

A typical securities firm's back office is characterized by multiple applications at various stages of their useful lives and not necessarily 'talking' with each other. Therefore STP would come to mean:

- Streamlining operational infrastructure (internal STP)

- Readying for connectivity with trade participants and matching utilities (external STP).

It is external STP that has lost attention following the postponement of the T+1 initiative. The case for internal STP is still alive, and expected to account for 50-70% of budgets for STP. Also, a company pursuing STP in its trading applications is also preparing itself for a more demanding time frame for trade settlement, the demand for which will eventually arise once the financial markets recover.

2. STP equals process automation

By definition STP envisages a seamless, automated and integrated transaction-processing environment. This cannot be achieved by just automating existing business processes. As is seen even in highly automated back offices, not all processes are at their most efficient due to duplication. Also existing automation, in most cases, will not maximize overall business process efficiency. So it is not possible to crash processing time further by increasing automation.

An STP program defines the 'to-be' processes, which will help achieve specified business objectives. This necessarily involves redesigning underlying processes and in the process opens up new routes to automation. STP therefore goes beyond process automation and in fact will involve reengineering of business processes.

3. STP is mainly an information technology solution

An obvious corollary to the proposition that STP goes beyond mere process automation is that STP is not just an IT issue. Implementation of STP is driven by business considerations such as reduction in processing costs, improvement in data integrity and usage for decision-making.

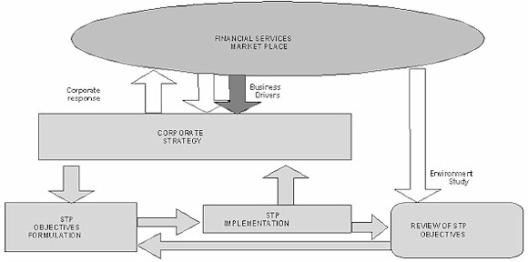

A typical STP program will begin with the definition of STP objectives, which are driven by business considerations aimed at improving top and bottom line. The STP component chain is illustrated in Figure below.

It is clear that business knowledge plays a key role. A successful STP program will bring together the best of knowledge and practice from business and technology domains.

4. STP is useful primarily for cost saving

The benefits of STP are generally considered to be:

- Reduction in costs, due to a reduction in process inefficiencies and release of manpower

- Reduction of risk, due to more efficient settlement and reconciliation as well as reduced exposure period when the settlement cycle is compressed

Both of these contribute to the bottom line of the company, and the general tendency is to measure the success of STP initiatives based on this. However the real measure of success is its impact on the competitive position of the industry participant. Cost is only one dimension of competitiveness. A well thought out STP strategy can aim to improve top line and margins. This could be in terms of:

- Improving service levels to customers

- Improving data or information usage efficiency

- Release of resources to more core functions

- Enhancing processing throughput.

The benefits of STP go beyond cost savings. It is a strategic imperative that enhances a firm's corporate performance and its competitiveness.

5. STP is all about the trade life cycle

STP is usually associated with the securities market trading cycle and this causes STP to be viewed only in the context of the trading process 'silo'.

However the concerns that STP seeks to address, such as inefficient processes and manual interventions, are equally prevalent in non-trade processes. For example, if an asset management firm improves its client record keeping process using STP, there are tangible business benefits both in terms of cost savings and improving service delivery.

There is an even better business case for any securities trading firm, because there are always several interacting processes that, along with trading, forms the core set of operations. For instance, will improvement in trade processing make much sense if reference data is unreliable?

Will improvement in failed trades processing alone suffice when the risk management process remains inefficient? In the interest of improvement in overall return on investment, STP must not be confined to the trading processes domain, but must extend to other supporting processes.

6. STP is a one shot exercise

The market place is dynamic and there could be external factors that can influence STP needs - for instance competitive pressure, new technologies and market regulations. This would necessitate revisiting the STP objectives and formulating new programs accordingly. The STP program structure should therefore provide for a feedback mechanism from key business and technology stakeholders so that the STP objectives can be kept in line with contemporary business strategy.

7. Current environment is too adverse for STP and related IT investments

Considering the scale of investment in STP, will it be possible to implement such a massive plan in the current period, when budgets are tight and corporate performance is lacklustre? There is a tendency to postpone an STP plan for better times.

The advantage of embarking on an elaborate STP exercise is in having control and direction over the whole implementation and thus efficiently planning and deploying resources. The flip side is the large budget commitments to be made and difficulty in measuring ROI, given the scope, scale, interdependencies and long implementation period. In the current environment, it may be better to take an incremental approach by

- Conducting firm-wide analysis for all core processes

- Phasing out affected processes in two or three buckets

- Selecting critical processes that will provide maximum business impact in phase one.

However, much hinges on careful and intelligent choice of target processes. Again it is necessary to have a pan-organizational view to take care of consistency and related dependencies.

A significant risk is that the sum of the individual (silo) savings or benefits will not equal the overall benefit, as there would still be bottlenecks in interfacing processes that have been excluded from scope. Some of the advantages of an incremental approach are:

- It can provide early and quick wins.

- With smaller outlays expected, it is easier to 'sell' internally to stakeholders while seeking funding

- It de-risks the implementation by phasing out changes

- It serves the interest of change management by gradually building organizational acceptance.

In summary

STP is a critical competitive weapon in the financial services industry. The key driver has always been business needs and therefore firms should not view STP narrowly as an IT solution. Its influence stretches far beyond the trading realm of operations and, when intelligently applied, STP will have a favourable impact on costs as well as the top line.

The indefinite postponement of the T+1 initiative has in no way negated the business compulsions leading to the STP solution. In fact, firms should use the time gained to focus on internal STP and, in the process, adequately meet any external STP challenges as and when they arise.

About Author: Deepak Pareek is a seasoned Financial Technology Specialist specializing in Enterprise, Internet, and Wireless applications. He has worked with a wide range of companies, financial institutions, and IT personnel to effectively meet the benchmarks. Deepak is available to consult on your next IT project e-mail him for additional details.