|

|

| themanager.org | Search | German Portal | Bookstore |

|

|

Findings indicate that co-movements among the U.S., Germany, and Japan markets are significant. Burhan F. Yavas, PhD

Graziadio Business Report,

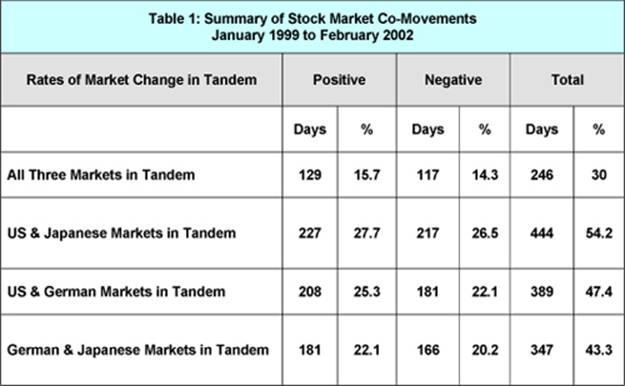

2007, Vol. 10, Issue 2 It is well known that stock market investing is risky. Both practitioners and theoreticians recommend holding a well-diversified portfolio to reduce risk. While mutual funds offer a quick and relatively inexpensive way to diversify, the purpose of this article is to address the issue of risk reduction through international diversification.[1] The article also provides support for the hypothesis that international market correlations increase after unexpected exogenous shocks. The implication is that diversification benefits may be reduced after such events. The tests of stability of market co-movements are based on before and after analyses of the September 11, 2001, terrorist events in the United States. The paper considers an important problem that may interest retail and institutional investors, portfolio managers, corporate executives and policy makers. Knowing the correlations between the returns of various national markets is important for the process of allocating investments among these markets. All of the major U.S. indices ended the year 2006 having logged double-digit gains. However, even though Standard & Poor's 500 index turned in a 13.6 percent performance, an investor would have done better had he or she ventured outside the U.S. Using averages, domestic stock funds gained 12.6 percent in 2006 compared to 25.5 percent for international stock funds Not surprisingly, Charles Schwab, a leading U.S.-based broker, recommends that its customers rebalance their portfolios in favor of foreign equities.[2] Many other financial advisors are also advising their clients to consider investment opportunities in overseas markets. While these recommendations by brokers may be specific to the current market conditions, globalization aided by advances in communication technology, abolition of capital and exchange controls, and deregulation in recent years, seem to have increased access to foreign markets. CAPM and MPT Theories of Finance Two well-known theories in the finance literature, the Capital Asset Pricing Model (CAPM) and the Modern Portfolio Theory (MPT), suggest that individual and institutional investors should hold a well-diversified portfolio to reduce risk. An institutional investor can achieve a well-diversified portfolio because the amount of funds in the portfolio is large enough for in-house diversification. Individual investors with limited wealth will have to find another way that does not require substantial funds to diversify their portfolios. Mutual funds offer a quick and relatively inexpensive way to diversify for small investors and others. It is also argued that since differences exist in levels of economic growth and timing of business cycles among various countries, international portfolio diversification can be used as a means of reducing risk. In fact, the 1990s witnessed an explosion of international portfolio investment, especially among emerging markets. Mutual fund companies such as Janus and Templeton achieved phenomenal rates of return on their investments during the mid to late 1990s. It should be made clear that while performances of these mutual funds over the long haul vary, it is still true that diversification reduces risk at a given level of return. Market Integration Influences National economies have recently become more closely linked, not only because of growing international trade and investment flows, but also due to terms of international financial transactions. Influences contributing to an increased general level of correlation among markets and markets integration include the following: 1. Development of global and multinational companies and organizations, 2. Advances in information technology, 3. Deregulation of the financial systems of the major industrialized countries, 4. Explosive growth in international capital flows, and 5. Abolishment of foreign exchange controls. While some controversy exists among investment professionals regarding the benefits and costs of international portfolio investment, there is agreement that international equity portfolio diversification recommendations are based on the existence of low correlations among national stock markets. On the other hand, if it is true, as some recent studies have shown, that cross-country correlation is increasing, due perhaps to the growing interdependence among the international markets, then benefits of international portfolio diversification may be overstated. In this article we aim to shed light on international equity market interdependence by utilizing data from three major equity markets for a relatively short time period. In examining the co-movements of American, Japanese, and German equity markets, we seek to identify diversification opportunities for international investors with the aim of lowering the investment risk. We also investigate the stability of the relationships among the markets after an unexpected, exogenous event. Research on Markets Research reveals that stock markets across the world are becoming more integrated. Madura found that correlations markedly increased over time.[3] Forbes and Rigobon tested the stock market contagion during the 1997 East Asian crisis, the 1994 Mexican Peso collapse, and the 1987 U.S. stock market crash.[4] Research on the stability of market integration, on the other hand, indicates that volatility affects cross market correlations. Interested readers should consult Longin and Solnik[5] and Meric and Meric.[6] Their results indicate that the co-movements of equity markets increased significantly after the crash, implying that the benefits of international diversification decreased considerably. Data and Methodology We use the daily closing values of the Standard & Poor's 500 Index (S&P 500), the Nikkei 225 Index, and the DAX 30 to represent the respective stock markets of the U.S., Japan, and Germany during the period of January 4, 1999 to February 28, 2002. First, we examine trading in Japan, followed by the opening of the markets in Germany after the close of the Japanese market. The German market has a one-hour overlap with the U.S. stock market. Therefore, global information is already incorporated in the non-U.S. markets prior to the opening of the U.S. market. However, the developments in Germany and in the U.S. are not reflected in Japan until the following day. We next focus our attention on the influence of the German market on that of the U.S. We close the loop by studying lagged correlations in terms of the U.S. market's influence on Japan and Germany. Findings and Results A simple analysis of data indicates that during the study period (January 1999 to February 2002), the three markets moved in tandem 30 percent of the days (15.7 percent positive and 14.3 percent negative). American and German markets moved concurrently 47.4 percent of the time, and Japanese and German markets moved in the same direction 43.3 percent of the time. Finally, the U.S. and Japanese markets moved together 54.2 percent of the time (See table 1).

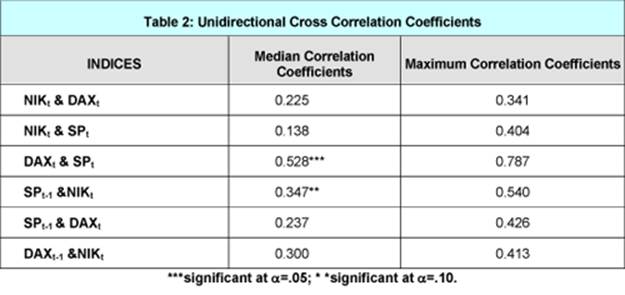

After observing the market co-movements in the same or in different directions, we calculate both auto and cross-correlations and conduct tests on the hypotheses to study whether they are statistically significant. If they are significant (that is, significantly different from zero) this will point to the direction of close correlation among the markets, a finding which implies diminished diversification benefits for investors. If, on the other hand, correlations are insignificant (not significantly different from zero), investors can benefit from international diversification. The results indicate that the Unidirectional Moving Correlation Coefficients (UMCC) of NIKt and DAXt are not significantly different from zero (Table 2). In plain terms, Japanese and German markets are not correlated. The implication is that both Japanese and German investors can realize diversification benefits by investing in each others' markets. We also note that the UMCC of Japan and the U.S. is likewise insignificant, implying that the American and Japanese investors may lower investment risk by investing in each other's markets, however, we also note that correlation coefficients have been increasing since the year 2000, indicating growing interdependence between the U.S. and the Japanese markets.

Looking at correlations between the German and the U.S. markets, we note that the correlations are significantly different from zero and show an increasing trend, a finding that implies that the co-movement (or interdependence) of the two markets has increased over time. Therefore, from the perspective of the international investor, these results imply that the benefits of international portfolio diversification across the U.S. and Germany are possibly becoming less significant. Nevertheless, it may be noted that the existence of past correlations does not guarantee that such correlations will exist for any future period. It is also interesting to note that since correlation coefficients are unidirectional, correlations going from the U.S. to Japan are not the same as those going in the opposite direction. This is due to the fact that trading hours of the markets are different and that the market that opens later typically contains information on what happened in the market or markets that had already closed. For example, we found the median correlation coefficient moving from the U.S. to Japan to be equal to 0.347, while the mean UMCC from Japan to U.S. is only .138. This result may indicate that the Nikkei 225 returns are much more correlated with the S&P 500 returns after the close of the U.S. market than would be the reverse case. Similar results were found between the U.S. and the German markets where mean UMCCs were higher in the direction from Germany to the U.S. than they were from the U.S. to Germany. This result again reflects the availability of information in the German market that opens well before trading in the U.S. begins. In conclusion, international diversification will result in risk reduction for a given return as long as the correlation coefficient between the domestic and the foreign market is less than one (i.e., less than 100 percent). Lower future correlation will provide deeper risk reduction. Based on our results, a U.S. investor having a portfolio of U.S. stocks will experience a small diversification benefit (risk reduction) by investing in German stocks since the cross correlation coefficients with the German market are rather large. On the other hand, the same U.S. investor will have better diversification benefit by investing in the Japanese market. The same is true for a German investor. This is so because a Germany-Japan combination will yield better diversification than will a Germany-U.S. combination. Similarly, investors in Japan can achieve equally desirable portfolio diversification benefits when they invest in Germany or the U.S. ---------------------------------------- [1] F. Rezayat, B.F Yavas. "International Portfolio Diversification: A Study of Linkages among the U.S., European and Japanese Equity Markets," Journal of Multinational Financial Management, 16, no. 4 (2006/10): 440-458. [2] L. Sonders. "Best Ideas for 2007 and Beyond: Be the Smart Money," Charles Schwab & Co., Inc., (December 2006). [3] J. Madura. International Financial Management, 3rd ed, (Minnesota: West Publishing Company, 1992). [4] K. Forbes, R. Rigobon. No Contagion, Only Interdependence: Measuring Stock Market Co-Movements, (Massachusetts: National Bureau of Economic Research, 1999). [5] Francois Longin, Bruno Solnik. "Is the Correlation in International Equity Returns Constant: 1960-1990?" Journal of International Money and Finance, 14, no. 1 (Feb, 1995): 3-26. [6] G. Meric, I. Meric. "Co-movements of European Equity Markets Before and After the 1987 Crash," Multinational Finance Journal, 1, no. 2 (1997): 137-154. This article first appeared in Graziadio Business Report, 2007, Vol. 10, Issue 2

|

Management Books worth reading now

|

||||||||||||

|

|

||||||||||||||

| up ñ | back to publications - Management and Strategy | back to themanager.org |

If you have questions or comments to our website, do not hesitate

to contact us (comments and questions are always welcomed):

webmaster2 AT reckliesmp.de

Copyright © 2001 Recklies Management Project GmbH

Status: 01. Juli 2015